Our pay cycles are stuck in an analog system

Over the last 50 years, the world has drastically shifted from analog to digital systems. There is no greater evidence of this impact than in our financial services. Gone are the paper checks and envelopes full of cash (and sadly the lollipops) bank tellers once slid across gilded counters or via seemingly futuristic drive-thru airvac tubes. But, you may be shocked to learn that the underlying system we use to transfer money between financial institutions—thus paying workers—remains largely unchanged from that bygone era. A courier no longer delivers a physical ledger to the bank, but the process by which those transfers are completed still takes days (typically 2-5). Paperwork also contributes to lag time; employers often require timesheet submissions many days ahead of the pay cycle, giving banks, and payroll companies, the time they need to clear and disburse funds to bank accounts. While this system once made our lives easier—when was the last time you had to visit a physical bank branch—it ultimately has not kept pace with the speed of work.

As our lives have increasingly digitized, so has the data we produce. Employment data has the potential to open up new financial services like earned wage access, ending the two-week pay cycle as we know it.

A paystub that meets the moment

Modern paystubs offer granular data, like hours worked, pay rates, job title, years employed, etc. That information can be utilized for daily or even hourly payouts, giving workers the wages they’ve already earned as they earn them.

Until recently, even online paystubs were read in PDF form (essentially digital paper). Through data standardization, and an extensive network of over 1.75 million employers and over 400 payroll companies, Argyle has created a digital paystub—a modern alternative that’s compatible with the way lenders use paper paystubs and PDFs today. Digital versions carry the same critical data in a comprehensive, itemized list, without all the hassles, slowdowns, and errors that come from manual workflows and third-party OCR services.

Digital paystubs are another piece of technology that is quickly advancing banking tools, moving all of us closer to financial solutions that meet the needs of the way we live and work today.

New financial tools for modern life

Living paycheck-to-paycheck is all too familiar for a majority of Americans, yet our financial institutions have done little to bridge the gap for those that need to cover basic daily expenses.

Over half of all households in the United States cannot cover a $1,000 emergency expense, according to a new BankRate survey conducted in January of 2022.

Fintechs and neobanks are stepping in to fill the gaps that predatory payday lenders existed in—which, for consumers, often results in an untenable debt spiral, borrowing against a future paycheck at astronomical rates.

Enter worker-centric liquidity solutions like paycheck-linked lending, earned wage access, and cash advances—sometimes known as early wage access, a contemporary form of cash advance—modern financial alternatives that are collectively upending bi-weekly paychecks.

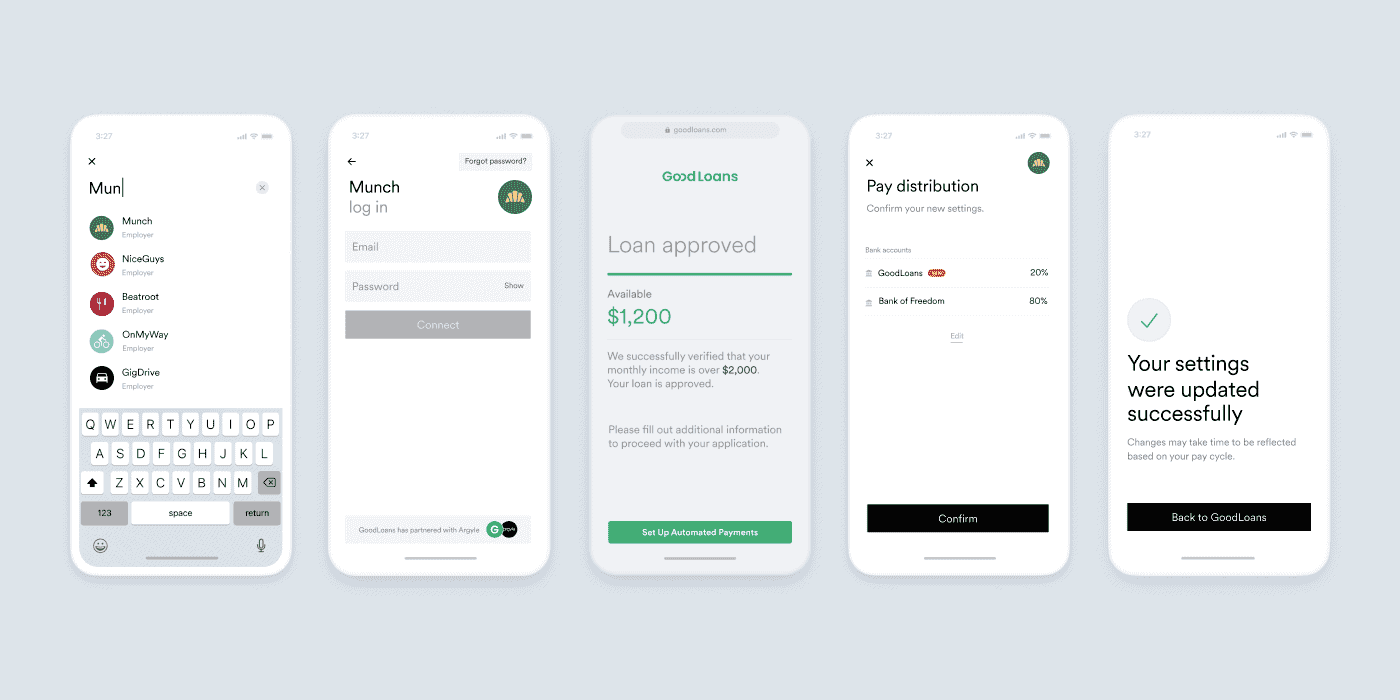

What is paycheck-linked lending?

In essence, paycheck-linked lending is a loan that relies on securing repayment directly from a borrower’s paycheck, providing a less risky payment method to underwrite—a borrower’s actual earnings rather than a static snapshot of a borrower’s bank account balance.

With paycheck-linked lending, payments for a loan are automatically withdrawn from the borrower’s paycheck, reducing the risk of default by 60% versus traditional ACH debits, which can take days to move funds from the borrower’s account to the creditor (increasing the chances of delinquency). Because defaults are reduced by nearly 2/3rds with paycheck-linked lending, this is a game changer for both consumers and lenders with the potential to expand financial access, offer lower interest rates, and maximize revenue by significantly decreasing defaults.

Dive into our white paper to learn more about paycheck-linked lending.

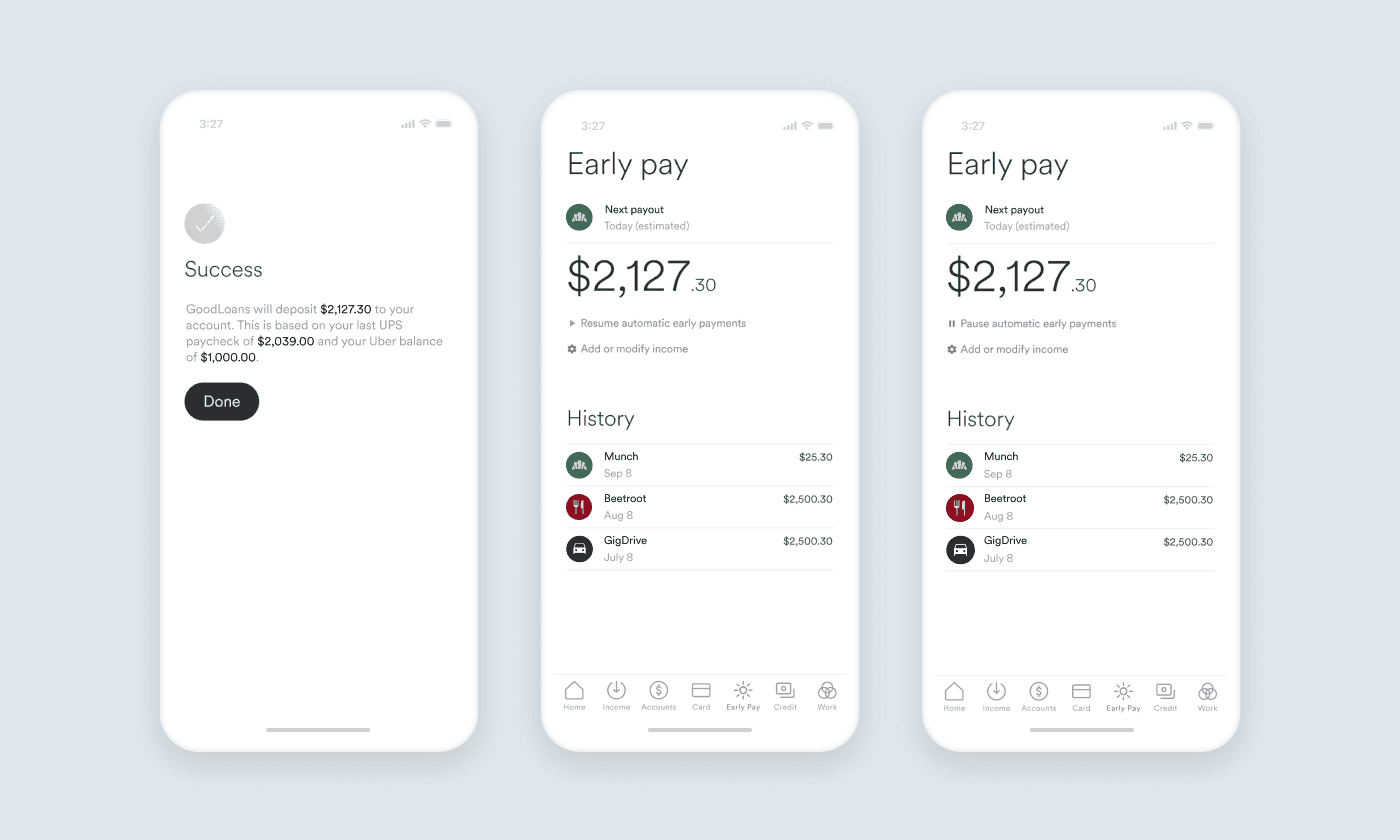

What is earned wage access?

For decades, service industry workers have enjoyed the benefit of taking home cash—part of their wages—at the end of their shift, traditionally in the form of tips. Think of this as an early form of earned wage access (EWA). Instead of putting in 40 or 80 hours and then receiving wages one to two weeks after you’ve actually earned them, wages may be accessed on an hourly or daily basis.

Providing money already earned can be critical bridge funding for workers who need to cover bills, medical costs or emergency expenses. Many employers are partnering with neobanks and EWA fintechs to offer employees partial payout of their earned wages as an employee benefit—typically at no cost to the employee. For workers whose employers don’t offer EWA as a fringe benefit, several innovative companies offer EWA at low interest rates (0-1.5%) or ask for a service gratuity.

While EWA is in its infancy, it is laying new piping over our existing financial plumbing that will inevitably change our understanding of pay periods and modernize our perspectives on payouts. EWA has the potential to significantly help workers budget in a subscription economy where consumers must navigate an avalanche of due dates corresponding to signups, not paydays.

With Argyle, your customers connect their payroll accounts directly to your application, for real-time visibility into earned-but-not-paid wages. With detailed shift data down to the hour, you can advance funds with confidence.

Curious to learn more about earned wage access? Contact an Argyle rep today.

What is cash advance / early wage access?

The traditional form of cash advances is payday loans—often predatory in nature, charging exorbitant interest and hefty fees for missed payments. Payday loans have earned their reputation, with the average APR nationally coming in at 400%. 16 states currently have laws against them and many others have tried to impose laws to regulate the high fees and interest rates associated with payday loans.

A new form of cash advance is taking root as early wage access. Early wage access differs from earned wages in a few ways; typically, early wage access is offered by a neobank where the consumer has an account and is tied to ACH direct deposits that a bank can verify. Consumer are granted funds two days prior to payday, at no cost. Because of the way ACH deposits transfer, banks are fully aware and certain these funds are coming, assuming virtually zero risk in offering early pay. Some consumers see this as a perk when their funds are running low near payday. However, early wage access essentially offers the same pay cycle—two weeks—and thus is the least disruptive of the current pay model.

A new ear for consumer finance

Paycheck-linked lending, early wage access, and early pay/cash advance opens the door for lenders to offer more credit options to borrowers who might otherwise turn to predatory lending practices, at rates significantly lower than existing bridge options. These loans not only open up a whole new line of business for lenders but also present a better borrowing opportunity for individuals turned away from conventional credit products.

Ready to move past archaic lending? Argyle can help you embrace the security of continuous access to income and employment data while providing the next generation of financial products. Contact an Argyle rep today.